If you’re just here looking for the Wealthsimple Trade referral code to receive the current promo (often to receive the cash value of free stock), the code is:

KYGLHAA few notes:

- If you don’t enter the referral code during account creation, you normally have up to 30 days to enter the referral code after creating your Wealthsimple Trade account. This can be done in the Wealthsimple Trade phone app by clicking the little gift icon.

- You MUST create a Personal (non-registered) Trade account. You can also create a TFSA and/or RRSP if you’d like but you MUST create the Personal account, as Wealthsimple will not deposit your bonus to a TFSA/RRSP account (you can transfer it manually via the phone app after a week or so if you’d like).

- You MUST fund your Trade account. Even $1 should be sufficient. I funded my Personal account and then waited for the bonus to arrive to be on the safe side before doing anything else (which took under 48 hours if I remember correctly though Wealthsimple says “within 7 days” as of early 2022).

- When you receive your cash bonus, you must keep it in Wealthsimple for at least 90 days. In other words, you can’t just create an account, get the bonus, immediately withdraw the bonus, and close your account.

- As far as the value of the random cash bonus you receive goes, according to Wealthsimple as of early 2022 the minimum bonus was $5, the average bonus was about $15 and only 5% of people managed a bonus worth over $50. No guarantees here, and YMMV. Assuming a bonus program is currently live, treat the bonus as a bonus, and you won’t be disappointed.

Enjoy!

If you arrived here looking for a little more information about Wealthsimple, I’ll start with the basics and then move on to pros/cons. No, it’s not for everyone. But it made sense for me. So here we go!

Who is Wealthsimple best suited towards?

In my view, Wealthsimple is best suited to the small retail investor – particularly the novice investor who is just getting started with investing or stock trading.

Why? They don’t charge trading fees on Canadian stocks: if you want to buy 1 share of TELUS and the share price is $32.29, you pay $32.29. You will collect dividends as time goes on, and if the stock price climbs to $65.45 in the future and you sell, you get that $65.45. If you want to buy USD stock, you pay a 1.5% premium on the exchange rate but it otherwise behaves the same.

This approach makes stock trading very accessible to investors who are just starting out and might only have $35 to invest today… using a different broker where they might have to pay a $1-50 trading fee just wouldn’t make sense.

Wealthsimple also makes the process of purchasing shares pretty easy – instead of the complex interface shown by some other brokers, Wealthsimple has opted for a simple one that is easy to use and understand. I’ll show a couple screenshots later so you can see what I mean.

Getting the negatives out of the way – the weaknesses and flaws of Wealthsimple

I’ll start with the negatives this time around, and finish off with the positives. I’ll try to be thorough and a little nit-picky for those who want as many details as possible.

The initial “new-user” experience isn’t nearly as smooth as it could be…

Note that most of my experience is with the desktop website – my use of the phone app is minimal (some things do require it though). In any case, some of the UI-specific issues I hit may be website-specific.

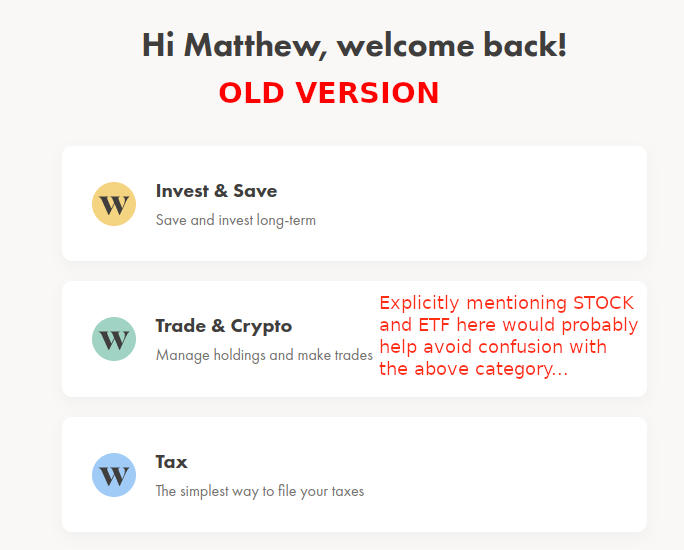

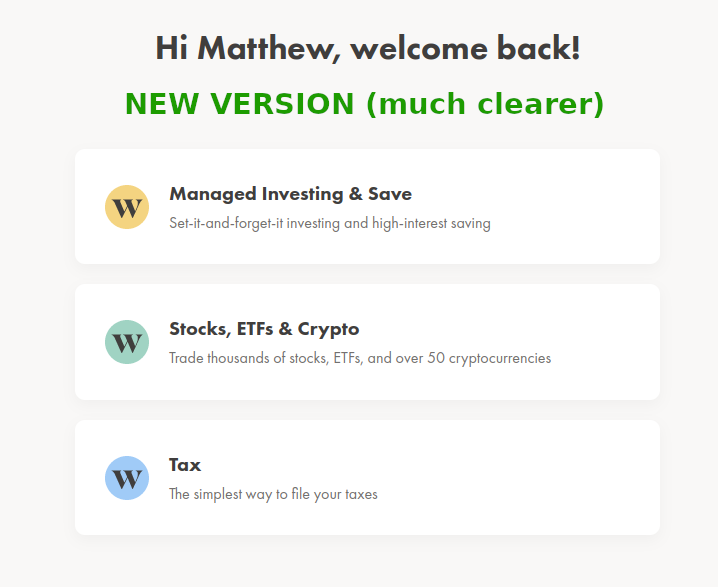

1) Wealthsimple offerings are currently broken down into 3 separate sections on the website (4 different Apps on the App Store although app merges may be coming soon). This could probably stand to be cleaned up a bit. Descriptions on the desktop site could use improvement. (FIXED) You can click the images for larger versions if curious.

2) Linking a bank account to fund your Wealthsimple account involves providing your bank account login credentials by default (via a service called Plaid). For many, this is a major cause for concern as compromised bank account credentials can have catastrophic implications – there is a reason that banks are none-to-thrilled about people sharing bank login details. However, note that if you select a bank (TD for example) and then cancel the process it does give you the option to use a more standard direct-withdrawal method (where you provide the bank/transit/account numbers that can be found on a voided cheque through any bank) which is arguably much safer and should probably be offered as an option up-front. Interac e-Transfer does not exist as an option – unfortunate because it would be a much faster and safer way for someone to get their feet wet who isn’t yet ready to commit to providing more thorough bank access.

3) The initial stock bonus (if applicable) doesn’t state why it can’t be transferred from your Personal account to a Registered account for a few days (“$0 available”), nor does it give an indication as to when it will be available for transfer. Having a visible ETA for any/all holds would be ideal.

4) Once numerous transactions have taken place, an expanded “Activity” history on the desktop website will collapse every few minutes, making it very challenging to sift through history that is more than 21 transactions old. If you plan to keep a separate log of your transactions elsewhere, consider starting your log from the get-go – if you wait until you have dozens/hundreds of transactions you might find the process to be rather frustrating. Note that this appears to be a desktop-only issue – I did not experience it during a quick test of the mobile app.

5) A number of items available in the mobile app aren’t available on the desktop website. A few that I’ve noticed: transferring funds between accounts (Personal to Registered for example), updating your mailing/physical addresses (incidentally, there may be a bug where they’re reversed on the backend – mail I received was addressed to my physical address instead of my mailing address), and the lack of a Discover section on the Desktop (including the ability to see a stock list limited to stocks that support Fractional Shares).

6) If you own both Telus (TSX Symbol: T) and AT&T (NYSE Symbol: T), when you receive dividends currently both of them will simply show up as having come from “T” which can make dividend tracking a little more challenging – you’ll have to simply remember that Telus dividends are paid on the 2/5/8/11 months, whereas AT&T dividends are paid on the 3/6/9/12 months. This likely applies to other stocks with shared symbols… Loews (NYSE:L) and Loblaw (TSX:L) as another example.

No options trading, no margin accounts – you can buy/sell stock (or ETFs) and that’s about it – this aspect of Wealthsimple might be a little too simple for veterans

To be clear, this isn’t necessarily a weakness. While a casino can vaporize your life savings – options trading can do it faster. Margin is an opportunity to see how a market crash + mathematics can liquidate everything you’ve invested. You can absolutely make the case that putting these tools in the hands of new investors is more likely to end badly than it is to end well.

With that said, on other platforms some people will buy Put Options as downside insurance, and selling Put Options can be a rational way to either get a stock you were interested in at a discount or earn a premium. Cases can be made where margin makes sense. Not having these tools available on Wealthsimple means that some investors may “outgrow” Wealthsimple.

It’s always possible these items may be added in the future: for Wealthsimple, options fees and margin rates would undoubtedly be lucrative. However, if these are items you want access to in the here-and-now, you’ll have to scratch Wealthsimple off your list.

UPDATE: Wealthsimple has added the ability to trade options.

1.5% foreign exchange fee (purchasing US stock)

I won’t be too hard on Wealthsimple here: unless they plan to rely on perpetual cash infusions from Ryan Reynolds (https://globalnews.ca/news/7829030/wealthsimple-financing-deal-drake-ryan-reynolds/) and other Venture Capitalists, they need to either get acquired, or make money someday. Somehow.

With essentially 0 fees otherwise, it’s really hard to pick on Wealthsimple over a fairly mild 1.5% foreign exchange premium that only applies to the purchase/sale of USD stocks (USD dividends appear to be exempt). After all, 1.5% is less than most bank and credit card forex rates in Canada (2.5% is common). And if you actually do plan to trade USD stocks frequently, you have the option of subscribing to Wealthsimple Plus for $10/month to get a USD account which can help reduce the costs of frequent USD trading.

With that said, there are other brokers that either charge low foreign exchange fees, have no foreign exchange fees to begin with (making their money elsewhere), or allow for some trickery (journaling, Norbert’s Gambit) to avoid currency conversion fees – depending on your use-case they could be more cost-effective in the long run.

No DRIP (Dividend Reinvestment Plan) support

Some offerings on the stock market offer optional DRIP enrolment where dividends can be automatically reinvested in a stock. Currently, Wealthsimple does not support this. In many cases this isn’t a big deal: Wealthsimple offers commission-free trading and you can easily reinvest your dividends into whatever you choose manually.

However, in some cases, DRIP comes with a bonus (for example, at the time of writing AI.TO offers a 2% discount on shares via DRIP). Additionally, DRIP would skip any for-ex fee potential on a US stock repurchase with dividends. And of course, if your intention is to reinvest all your dividends into the originating stock, at the very least the lack of DRIP means you need to manually log in to reinvest.

Only Canada and US exchanges are supported

You’re probably in luck if you want to buy something traded on the TSX, CSE, TSXV, NYSE, NASDAQ, NEO, or BATS exchanges. There are some exceptions, but most of the stocks available on these exchanges are available via Wealthsimple.

If you were hoping to buy something on the London or Tokyo exchanges though, look elsewhere.

Wealthsimple is not a big established name with a history of profitability

I’m going to preface this by stating the following:

- Competition is good.

- Wealthsimple has a good offering.

- I’m glad Wealthsimple is in this space.

Keeping that in mind:

Wealthsimple was founded in 2014, merged with ShareOwner Investments in 2015, and is owned in large part by Power Corporation of Canada (who itself has a large ownership stake in major names like Great-West Life and Investors Group). In the grand scheme of things they’re relatively new. The Wealthsimple investing platform was still not profitable as of early 2021 ( https://www.theglobeandmail.com/business/article-wealthsimple-on-brink-of-largest-ever-canadian-private-tech-funding/ ).

Wealthsimple technically offers services/products via other affiliates. Wealthsimple Trade operations appear to take place under the ShareOwner name which seems to be regulated by the IIROC ( https://www.iiroc.ca/investors/choosing-investment-advisor/dealers-we-regulate/canadian-shareowner-investments-inc-wealthsimple-trade ). Wealthsimple itself claims not to be an IIROC member. Neither Wealthsimple nor ShareHolder appear to be CDIC member institutions, though cash balances from Wealthsimple Cash/Save are apparently held in trust at a CDIC institution.

There’s nothing inherently bad, wrong, or suspicious with any of these things: this is what you’d expect of a start-up in an industry with big powerful players. None of it is hidden, and much can even be found in the fine print on the bottom of their website.

The point I’m trying to get across is that Wealthsimple is not a big bank, nor are they a huge multinational conglomerate swimming in cash. There are pros and cons to that, which may affect your comfort level.

Getting to the Good

Despite a few of the pain points above, Wealthsimple actually has some really strong points.

Low (no) barrier to entry

0 account minimums, 0 account fees, no-commission trades. All you need is a bank account and some money. Heck, you could technically get started with as little as $1, and maybe even come back months/years later to find your investment has grown to $1.30. That’s not feasible with the majority of brokers. If you plan to start small, this alone might put Wealthsimple head-and-shoulders above the rest of the competition.

Buying and selling stock is pretty easy

An example screenshot is located below.

Find the stock you’re interested in, enter the number of shares you want, it’ll tell you the estimated cost, and you can click the “Buy” button. For those who know the lingo and want a little more control, Limit and Stop Limit orders are available as well.

Funding your account is fast… the 2nd time around

When you first create an account and add funds from your bank you’ll have a painfully long 4-5 day wait before your funds are available to spend. However, after that first successful deposit you’ll typically receive an “Instant deposit limit” of $200-$1500 (up to $5000 if you subscribe to Wealthsimple Plus) which results in no waiting time necessary. This is great if don’t want to keep cash floating in your Wealthsimple account, yet want instant availability of funds just in case the stock you want shows up at the right price.

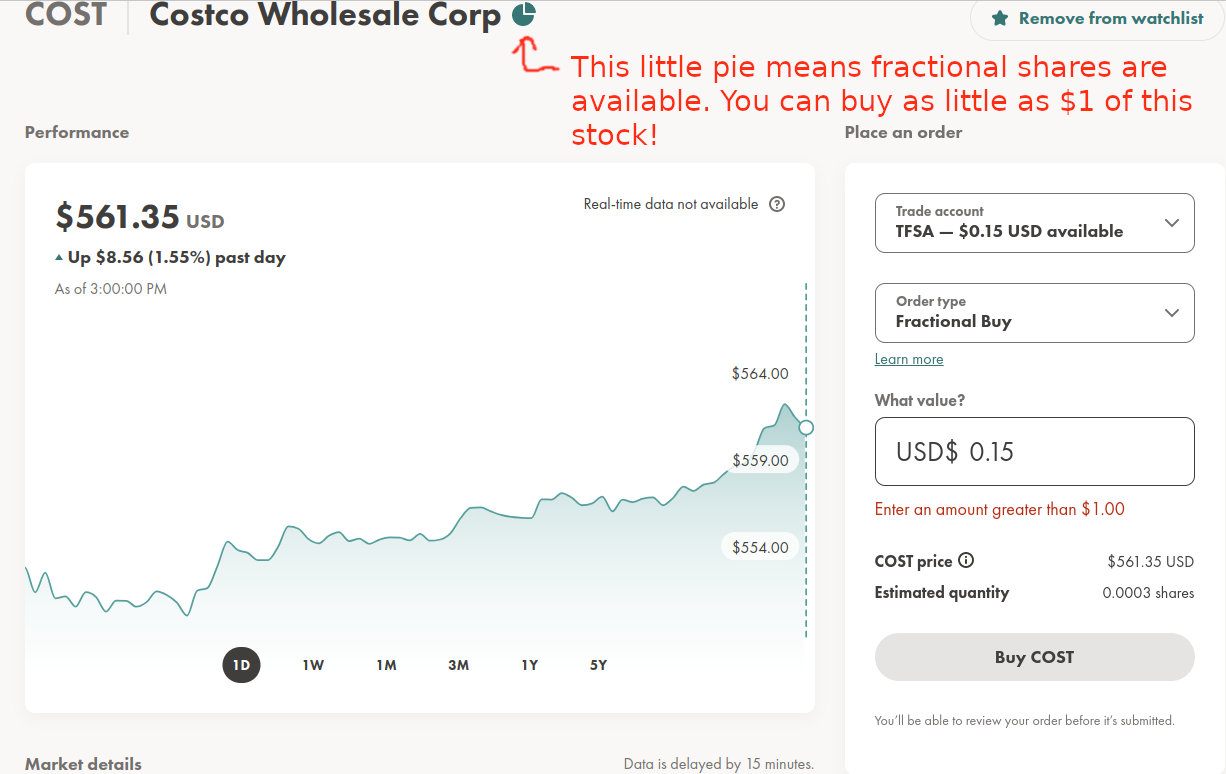

Fractional Shares

Sometimes a share is a little too costly – for example, in the example below I clearly don’t have the $561.35 USD necessary for the Costco share I want!

If you have at least $1 you can buy part of a share, known as a Fractional Share. If the stock pays dividends you’ll even get part of the dividend. The downside? Wealthsimple only places the fractional share orders once per day (about an hour before the TSX closes currently), so your order won’t execute until then and you’ll be buying/selling at whatever the share price happens to be at that time.

This is a great way to slowly pick up pieces of certain stocks you might want. It also provides an option for re-investing dividends – a $1.20 dividend probably won’t be enough money to buy a new stock that you want. But it’s definitely enough money to put into a Fractional Share.

Crypto availability

If you’re one of those who believe crypto is the future… it’s an option. If you’re one of those who believe crypto will inevitably fall to 0 but want to hedge a little bit of your portfolio just in case…. it’s an option. If you’re one of those who think it’s a great place for micro-trading… keep in mind that it’s subject to capital gains.

Bonuses

A major advantage to Wealthsimple being focused on growth is that they’ve offered various bonuses at various times. This has ranged from referral bonuses to free cash for using their tax software. Seriously, Intuit wanted me to spend $45 to use their tax software whereas Wealthsimple wanted to pay me. And why did I open a Wealthsimple Trade account? Because nobody else offered me $0 trading fees + the cash value of a free stock for signing up.

Wealthsimple Invest

If you later decide that rather than manually picking stocks, you’d rather go with a more simplified investing system where you make regular contributions and don’t have to worry about managing your portfolio (similar to mutual funds), you can use the Wealthsimple Invest service. It asks a number of questions to determine your risk profile, automatically constructs a profile for you, will automatically reinvest dividends and re-balance, and allows you to set up automatic deposits and contributions if you’d like.

Registered Accounts

Mentioning this last because… well… pretty much everyone has this available. RRSP and TFSA accounts are available in addition to the default “Personal” (non-registered) account.

With all that in mind, if you’re ready to open a Wealthsimple Trade account, feel free to use referral code KYGLHA (you typically have about 30 days after creating your account during which you can enter a code via the Gift icon in the phone app). Wealthsimple frequently changes the bonus program, but you’ll receive whatever the current bonus is. Note that you’ll typically need to fund your Personal Trade account (even $1 is usually sufficient), and the bonus will always be deposited in your Personal account – if you have a TFSA or RRSP account you can transfer it there a week later if you want – note that if you transfer to TFSA/RRSP it will be applied against your contribution room.